ScenarioMIP CMIP7: What Changes and What It Means for Finance and the Built Environment

An analysis of the new ScenarioMIP design for CMIP7 (Van Vuuren et al., 2026), and what it means for science, disclosure standards, banks, lenders and real estate..

The climate scenarios are being rewritten, and almost everything downstream depends on them

On 7 April 2026, Geoscientific Model Development published what reads, on the surface, as a piece of technical housekeeping: the design document for the next generation of climate scenarios. It is anything but. The Scenario Model Intercomparison Project for CMIP7, led by Detlef van Vuuren with several dozen co-authors across the modelling community, sets the terms for the simulations that will feed the IPCC's Seventh Assessment Report. Through that assessment, and through the integrated assessment models and simple climate models that translate it, the framework propagates into a remarkably wide apparatus: corporate disclosure standards, bank stress tests, mortgage and credit risk models, real estate stranding tools and national risk assessments. When the scenario framework changes, the inputs to a great deal of climate decision-making change with it, usually with a lag of several years and usually without the people relying on the outputs noticing the join.

The paper (Van Vuuren et al., 2026, Geosci. Model Dev., 19, 2627 to 2656) is the blueprint for that change. It is worth reading closely, because several assumptions the finance and built-environment worlds still treat as fixed are being retired. This piece sets out what the design actually does, then traces the consequences along the chain that runs from Earth system models to the spreadsheet a valuer or a credit officer opens on a Monday morning.

What the paper is

Scenarios are plausible, internally consistent descriptions of how the future might unfold: emissions, land use, the socio-economic conditions behind them, and the climate outcomes that follow (Van Vuuren et al., 2026). Under CMIP6, ScenarioMIP produced the set that became the backbone of the AR6 physical science assessment and then radiated outward into impacts research and, eventually, the financial sector (O'Neill et al., 2016; Tebaldi et al., 2021). ScenarioMIP for CMIP7 is the successor exercise.

The central constraint is unchanged. Earth system models are expensive to run and archive, so only a small set of scenarios can be simulated. The task is to choose a set small enough to be tractable but rich enough to serve three jobs at once: answering direct climate-science questions, feeding the impacts and mitigation communities, and supporting policy through the IPCC. The new design attempts this with seven core scenarios, developed through an unusually long and open consultation that included public review and a deliberately broadened advisory group.

Timing matters here. Earth system runs were planned to begin in spring 2026, with the first high-priority results arriving around mid-year, so that literature can appear across 2026 and 2027 in time for AR7. The IPCC Working Group reports are expected to begin emerging in mid-2028 and the Synthesis Report by late 2029, although the precise schedule has itself been contested within the IPCC and remained unresolved into late 2025 (IPCC, 2025; Carbon Brief, 2025). The practical implication is immediate: these are the scenarios the next assessment will rest on, but they will not displace the CMIP6 and SSP-RCP material in everyday professional use for some time.

What is genuinely new

Scenarios are named by emission trend, not by forcing level

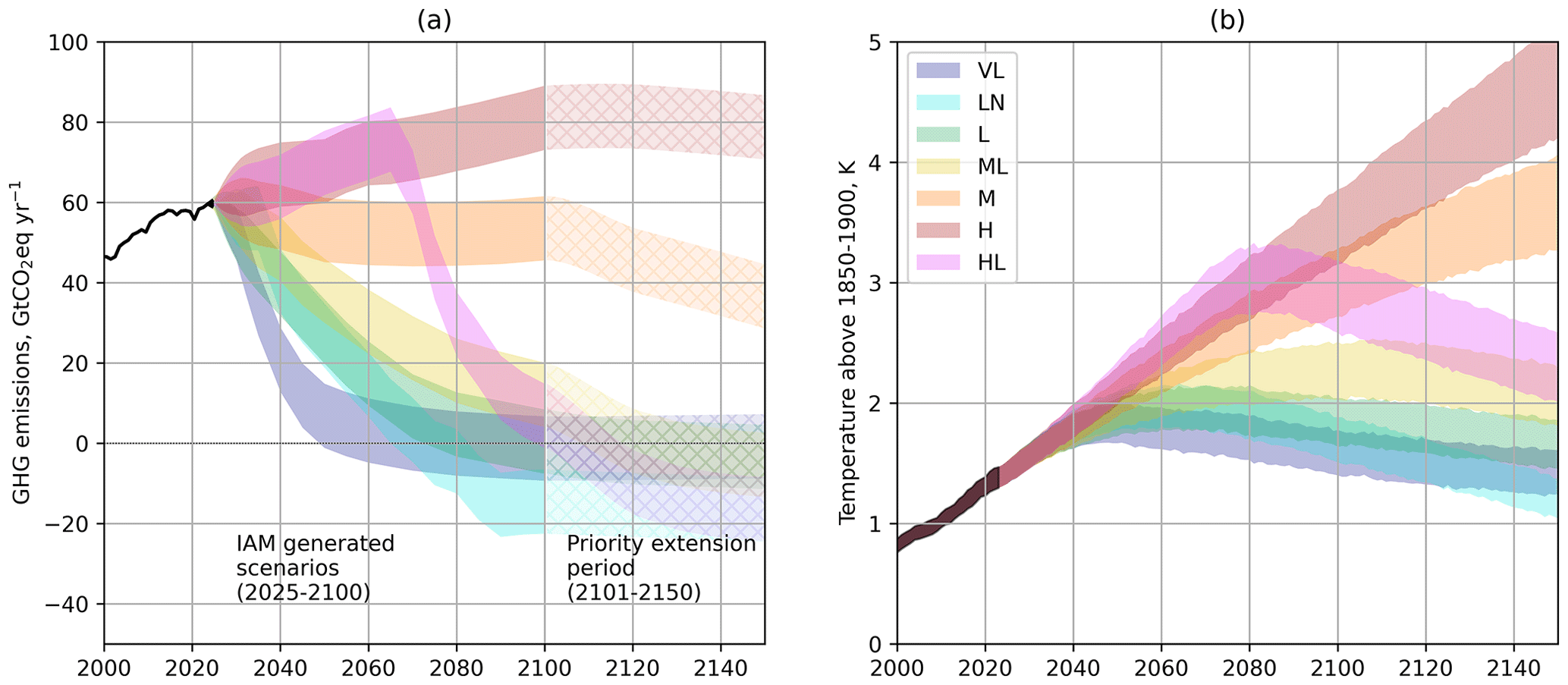

This is the change most likely to disrupt habits. The familiar CMIP6 labels (SSP5-8.5, SSP2-4.5, SSP1-1.9 and the rest) packed a socio-economic storyline and a target radiative forcing level into a single shorthand. The new set drops that. The seven scenarios are named after the shape of their emissions trajectory, and the resulting temperature is treated as an output of the model runs rather than a label fixed in advance (Van Vuuren et al., 2026). The seven are:

- High (H): emissions as high as still judged plausible, premised on a rollback of current mitigation policy. Expected to produce forcing below the old SSP5-8.5.

- High-to-Low (HL): tracks High to mid-century, then turns sharply towards net zero CO2 by 2100.

- Medium (M): the consequences of current implemented policies and trends simply continuing, with announced pledges not counted unless backed by policy.

- Medium-to-Low (ML): delayed strengthening of effort, falling short of Paris this century but reaching net zero CO2 by 2100 with modest net-negative emissions thereafter.

- Low (L): consistent with holding warming likely below 2 degrees C throughout, without returning to 1.5 degrees C this century.

- Very Low (VL): warming kept as low as plausibly achievable, with a limited overshoot and a return below 1.5 degrees C by 2100.

- Low-to-Negative (LN): a larger overshoot followed by sustained net-negative emissions, designed specifically to probe the reversibility of the climate system.

(Figure 1: Proposed scenarios for CMIP7 ScenarioMIP, showing (a) GHG emissions pathways as a function of time for each of the proposed scenarios (based on GWP-100) and (b) the associated global average temperature outcomes using the probabilistic FaIR ensemble used in IPCC AR6 (Smith, 2025; Smith et al., 2024). The shaded area for emissions shows ±8 GtCO2 around the expected marker scenario value while for temperature outcomes, it shows the 33–67 percentile range of the distribution for the same expected marker scenario. Data for the historical period can be found in Nicholls et al. (2025a). Scenarios are (H) High, (HL) High-to-Low, (M) Medium, (ML) Medium-to-Low, (L) Low, (LN) Low-to-Negative and (VL) Very Low. The final emission trajectories will depend on the finalized IAM runs but are expected to be roughly consistent with the illustrations provided here. The final temperature outcomes will be known only at completion of Earth system models' experiments, and will, for this phase of ScenarioMIP, include also the effects of carbon cycle feedbacks. Models are requested to run the scenarios for the period 2025–2150; the textured regions for the 2100–2150 period (AD) indicate that these emissions and forcings are defined in the extension protocol. Source: Van Vuuren et al. (2026))

The socio-economic storylines have not vanished. The Shared Socioeconomic Pathways remain in wide use, and the integrated assessment teams quantifying these scenarios mostly built on various SSPs because rich quantifications already existed (Riahi et al., 2017; Van Vuuren et al., 2026). What changes is the headline framing: the design deliberately separates the emissions pathway from any single climate outcome, because many socio-economic worlds can produce similar emissions, and the same emissions can later be paired with different development assumptions in impacts work.

The plausible range has narrowed at both ends

The high end has come down. The authors are explicit that the CMIP6 high-emissions level represented by SSP5-8.5 has become implausible, on the basis of falling renewable costs, the emergence of climate policy and recent emissions trends (Van Vuuren et al., 2026; Hausfather & Peters, 2020). The new High scenario is expected to sit below it. At the same time, the lowest CMIP6 trajectories have become inconsistent with observed emissions over the 2020 to 2030 period. The net effect is a compressed twenty-first-century range, with temperature outcomes expected to run from roughly 1.5 degrees C to almost 3.5 degrees C above the 1850 to 1900 baseline by 2100.

The design assigns no probabilities. The team treats plausibility as a subjective judgement and leaves the question of which futures are more likely as an open research problem, framing High and Very Low as "as high as plausible" and "as low as plausible" respectively.

Most scenarios will be run emission-driven, not concentration-driven

This is the most consequential technical shift. Until now, ScenarioMIP experiments prescribed atmospheric CO2 concentrations. For CMIP7, most simulations will instead prescribe CO2 emissions and let each model's own carbon-cycle representation determine the resulting concentration (Van Vuuren et al., 2026, building on Sanderson et al., 2024). The other well-mixed greenhouse gases stay on prescribed concentrations in the core experiments.

The pay-off is that carbon-cycle and climate feedbacks, and the real uncertainty in them, are now built into the spread of outcomes rather than assumed away. The cost is interpretability: the projected range will widen because models disagree about how much of a given emissions pathway stays airborne. To keep this legible, the protocol asks emission-driven groups to also run at least one scenario in concentration-driven mode for clean comparison, and it treats the drift between simulated and observed CO2 as a diagnostic of carbon-cycle sensitivity rather than an error to correct. For anyone working with model output downstream, the headline is that the next generation of projections will carry a visibly larger Earth-system uncertainty band, and that band will mean something.

Other shifts worth noting

The historical baseline jumps from 2015 (CMIP6) to 2023, with 2024 to 2025 held close to observed trends. That pulls the Covid-19 disruption and recent gas-market shifts inside the historical record and shortens the gap between when a scenario is built and when its early years are already in the past (Van Vuuren et al., 2026).

Overshoot, peak-and-decline and reversibility move to centre stage. Several scenarios are explicitly about peaks and declines, and the Low-to-Negative scenario is effectively a controlled experiment in climate reversal, a question the idealised emission-driven experiments behind the protocol were designed to probe (Sanderson et al., 2024, 2025). The long-term extensions now run to 2500 (against 2300 in CMIP6) to give the ice-sheet, sea-level and ecosystem communities time to study stabilisation and irreversibility.

Equity and justice are acknowledged, then deliberately left out. The authors accept the critique that IPCC-assessed scenarios have let global inequalities in income and energy use persist and have treated the sharing of mitigation, removal and adaptation effort too lightly (Zimm et al., 2024). But they argue this particular exercise, aimed at the broad global relationship between emissions and climate outcomes in a multi-model ensemble, is the wrong instrument for distributional questions, and they defer those to downstream research, pointing instead to process changes as their answer on the justice of the exercise itself. Whether deferral is adequate is exactly what the wider literature will continue to argue about.

Why this reaches far beyond climate science

The reason a model-design paper matters to a lender or a valuer is that climate decision-support runs on a transmission chain, and these scenarios sit at its source. The chain runs roughly as follows. Integrated assessment models turn scenario narratives into emissions and land-use pathways. Earth system models turn those into physical climate variables. Simple climate models and emulators, calibrated to the model ensemble, compress the result into the temperature and forcing pathways that non-specialists can use. The Network for Greening the Financial System (NGFS) then couples those climate and integrated-assessment foundations to macroeconomic and financial models to produce the scenarios that supervisors and firms actually run (NGFS, 2024; Banco de España, 2023). Disclosure standards sit at the end of the chain, requiring firms to use scenario analysis without prescribing a single source.

Two features of this chain matter for what follows. First, the financial layer does not consume IPCC output directly; it consumes the same SSP-RCP and integrated-assessment foundations, repackaged. The NGFS scenarios are explicitly built on the representative concentration pathways, the SSPs and the integrated assessment models behind them (Banco de España, 2023). For asset-level physical risk, practitioners more often reach past the NGFS to the SSP-RCP projections themselves, because those can be downscaled from CMIP ensembles to the resolution an individual asset needs (Munich Re, 2025). Second, because the chain is long, change at the source arrives downstream slowly and unevenly. That is why a 2026 design paper is best read as a multi-year transition signal rather than a switch.

Disclosure standards: ISSB, TCFD and TNFD

The clearest exposure is in disclosure. The International Sustainability Standards Board's IFRS S2 requires an entity to disclose its assessment of climate resilience and to use climate-related scenario analysis to inform that assessment, covering both physical and transition risks (IFRS Foundation, 2023; EY, 2023). At minimum a qualitative analysis is required, the ISSB has indicated where a Paris-aligned (1.5 degrees C) scenario is relevant, and it has acknowledged that off-the-shelf scenarios such as the NGFS set may be useful (IFRS Foundation, 2022). The board reaffirmed scenario analysis as a core requirement even after issuing targeted implementation amendments in December 2025 (Socious, 2026). By 2025, on the IFRS Foundation's own jurisdictional reporting as relayed in secondary coverage, more than 30 jurisdictions representing over 60 per cent of global GDP had committed to adopt or align with the standards, with requirements taking effect in a first wave of jurisdictions from 1 January 2026 (Sustainability Atlas, 2026; Socious, 2026).

This is where the new framework lands. IFRS S2 deliberately does not name the scenarios a firm must use, so the change will not arrive as a standard revision. It will arrive through the scenario libraries that preparers and their advisers actually pick up, and through the regulators that point to them. As the NGFS and the SSP-RCP projections re-base onto CMIP7, the "1.5 degrees C-aligned" and high-end scenarios that IFRS S2 resilience assessments lean on will quietly change shape: a lower and better-justified high end, a wider physical-risk band from emission-driven runs, and temperature read off the back of the models rather than fixed in the label. The methodological footnote in next year's resilience disclosures matters more than it looks.

TCFD's recommendations, which pioneered the four-pillar structure (governance, strategy, risk management, metrics and targets) and the resilience-through-scenario-analysis idea, were folded into the ISSB's monitoring remit, and the ISSB drew on TCFD material for its application support (IFRS Foundation, 2022). The lineage is direct, so the same scenario dependency runs through any TCFD-aligned reporting that persists in jurisdictions yet to move to ISSB.

The Taskforce on Nature-related Financial Disclosures extends the pattern into nature. Its LEAP approach (Locate, Evaluate, Assess, Prepare) culminates in a resilience disclosure, Strategy C, and the TNFD recommends integrated climate-and-nature scenarios, explicitly building on the market's experience with climate scenario analysis (TNFD, 2023a, 2023b). Because nature scenarios are being bootstrapped onto the climate scenario architecture rather than built from scratch, a re-base of the climate layer propagates into the nature layer too, and it does so while nature-scenario practice is still immature and therefore more easily reshaped.

Banks and lending

Supervisory climate stress testing is built on the same foundations, one layer further down. The European Central Bank's 2022 climate risk stress test used NGFS scenarios, calibrating its disorderly transition case on the NGFS delayed-transition pathway and its orderly case on NGFS Net Zero 2050 (ECB, 2022). The Bank of England's 2021 to 2022 Climate Biennial Exploratory Scenario took the NGFS Net Zero 2050, Delayed Transition and Current Policies scenarios as its starting point, expanding them with additional transmission channels and Met Office input (Bank of England, 2021). Industry commentary now describes NGFS scenarios as the default input for climate stress testing at the ECB, the Bank of England and many other supervisors (Continuuiti, 2026; Deloitte, 2022).

The physical-risk leg of these exercises reaches back to the IPCC pathways directly. In integrating climate risk into the 2025 EU-wide stress test, the ECB computed a granular, borrower-level physical-risk assessment for river flooding based on the IPCC's RCP4.5 scenario for 2021 to 2050, and combined it with the NGFS Nationally Determined Contributions scenario, with one analysis finding the flood overlay added roughly 77 basis points to banks' credit-risk losses (ECB, 2025). The Bank of England's 2025 climate-related financial disclosure similarly drew on CBES variable pathways, the NGFS Phase V Scenario Explorer and, tellingly for the built environment, the Energy Performance of Buildings Register, modelling expected credit losses through changes in probability of default (Bank of England, 2025).

For lending, three consequences follow. First, the transition-risk side runs through NGFS scenarios, so it inherits whatever the CMIP7 re-base does to the integrated-assessment and climate foundations the NGFS sits on, with a lag set by the NGFS update cycle (Phase V landed in November 2024). Second, the physical-risk side that drives mortgage and corporate credit overlays often uses SSP-RCP projections, so the narrowing of the plausible range and the move to emission-driven runs feed straight into flood, heat and subsidence modelling for property-backed lending. Third, and most pointedly, any credit or capital framework that has quietly used RCP8.5 as its conservative physical-risk anchor is now anchored to a pathway the source community treats as implausible, a tension addressed below.

Real estate

Property sits at the confluence of both risk channels, and the two run on different parts of the scenario machinery.

On the transition side, the dominant tool is the Carbon Risk Real Estate Monitor (CRREM), used by investors with well over 450 billion euros in assets under management (CRREM, 2023). CRREM derives building-level decarbonisation pathways by breaking the Paris-consistent global emissions budget down to countries, the real estate sector within them and individual property types, anchored to IPCC emissions pathways and the IEA's 1.5 degrees C Net Zero by 2050 roadmap, and aligned with the Science Based Targets initiative (CRREM, 2023; Greengage, 2023). A building "strands" when its carbon intensity crosses the declining pathway, with implications for valuation, lettability and compliance. Because CRREM rests on carbon budgets derived from IPCC pathways, a re-based assessment cycle eventually flows into the budgets and therefore into the stranding dates that increasingly drive retrofit sequencing and capital allocation in commercial portfolios. This is the channel closest to UK minimum energy efficiency standards and EPC-driven obsolescence, where the regulatory and the scenario logics already reinforce one another.

On the physical side, asset-level flood, heat, wind and subsidence risk is typically derived from downscaled CMIP projections under SSP-RCP pairings, because they offer the spatial resolution an individual building needs that macro-financial NGFS scenarios do not (Munich Re, 2025; JBA Risk Management, 2025). Here the CMIP7 changes bite directly. A lower and better-justified high end reframes the worst-case used in resilience and engineering-threshold work; the emission-driven approach widens the physical-risk band; and the explicit overshoot and peak-and-decline scenarios provide, for the first time, a defensible basis for assessing assets under trajectories that breach a warming level and then return, which matters for long-lived assets and long-tenor lending against them.

The RCP8.5 reckoning

Underneath all of this sits a debate the new framework effectively settles in practice. RCP8.5 was conceived as a high-risk, low-likelihood pathway, but for years it was widely treated as "business as usual," a usage Hausfather and Peters (2020) argued was misleading, warning that overstating the likelihood of extreme outcomes can make mitigation look harder than it is. The position was contested: Schwalm, Glendon and Duffy (2020) maintained that historical and near-term cumulative CO2 emissions tracked RCP8.5 more closely than the alternatives and that, for the purpose of driving climate models, total atmospheric CO2 is what counts. The IPCC's Sixth Assessment Report came down on the side of caution, treating the highest pathway as low-likelihood.

ScenarioMIP for CMIP7 formalises that judgement into the architecture rather than leaving it to interpretation: the new High scenario is designed to sit below SSP5-8.5 (Van Vuuren et al., 2026). For practitioners, the implication is not that tail risk has vanished but that the upper tail of the plausible range has moved, and that any analysis still using RCP8.5 as a default conservative case will increasingly need to justify the choice rather than assume it. The point applies with particular force to the long-horizon physical-risk work embedded in infrastructure, insurance and real estate, where RCP8.5 has been the habitual stress case.

The lag problem

None of this is a switch that flips in 2026. The CMIP6 and SSP-RCP material remains the working basis for tools, disclosures and stress tests today. The new output will trickle in from mid-2026, feed the literature across 2026 and 2027, and inform AR7 in 2028 and 2029, after which the NGFS, the supervisory exercises and the commercial data providers will re-base on their own cycles. The honest message for anyone maintaining scenario-based tooling is therefore twofold: treat current RCP8.5-anchored framing as something with a known expiry date, and plan the migration deliberately, because the chain is long enough that waiting for the change to arrive is the same as being caught unprepared when it does.

Tensions worth watching

A few open questions deserve to be carried forward rather than smoothed over.

The wider emission-driven range is a genuine improvement in honesty about Earth-system uncertainty, but it will be harder to communicate. A projection band that widens because models disagree about the carbon cycle is more faithful and less convenient, and there is a real risk of it being read as the science becoming less certain rather than more complete, especially once it reaches audiences several translations removed from the modelling.

Plausibility is doing heavy lifting, and the authors are candid that it is a subjective judgement, conditional in places on assumptions that are themselves hypothetical, including the assumption that the scenarios contain no climate impacts (Van Vuuren et al., 2026). Dropping SSP5-8.5 reflects a defensible reading of current trends, but it is a reading, and the framework's own caveat, that futures outside the range remain possible, deserves to travel with the scenarios into finance rather than being lost in translation.

The equity gap is unresolved by design. Deferring distributional questions to downstream research is coherent for a physical-climate exercise, but it answers a prominent critique procedurally rather than substantively, and the just-transition literature is unlikely to consider the matter closed (Zimm et al., 2024).

Finally, the twenty-first-century window keeps shrinking. Each CMIP cycle starts its future later, and this one runs its scenarios only to 2100 with stylised extensions beyond, because integrated assessment models reaching past 2100 were not ready in time. It is a reasonable pragmatic call, and a reminder that the scenario machinery is straining against its own timelines just as the demand placed on it, by disclosure standards, supervisors and markets, is rising.

The bottom line

ScenarioMIP for CMIP7 is the most consequential climate document most people in finance and the built environment will never read in full. It retires the high-end pathway that anchored a decade of worst-case thinking, rebuilds the scenarios around emissions trajectories and lets the climate outcome emerge from the models, opens up the carbon-cycle uncertainty that was previously fixed, and pushes overshoot and reversibility to the front of the agenda. For the science it offers a more honest, if messier, picture. For the ISSB resilience assessments, TNFD nature scenarios, bank stress tests, lending models and real estate stranding tools that depend on these foundations at second and third hand, it starts a clock running on assumptions, the RCP8.5 default chief among them, that have been treated as permanent. The work to update those tools does not start when AR7 lands in 2028 and 2029. It starts now, with the recognition that the ground beneath the scenarios has already shifted.

References

Banco de España. (2023). Conceptual underpinnings of the NGFS scenarios and suggestions for improvement (Occasional Paper No. 2302). https://www.bde.es/f/webbde/SES/Secciones/Publicaciones/PublicacionesSeriadas/DocumentosOcasionales/23/Files/do2302e.pdf

Bank of England. (2021). Key elements of the 2021 Biennial Exploratory Scenario: Financial risks from climate change. https://www.bankofengland.co.uk/stress-testing/2021/key-elements-2021-biennial-exploratory-scenario-financial-risks-climate-change

Bank of England. (2025). The Bank of England's climate-related financial disclosure 2025. https://www.bankofengland.co.uk/climate-change/the-bank-of-englands-climate-related-financial-disclosure-2025

Carbon Brief. (2025). Ongoing failure to agree AR7 timeline is "unprecedented" in IPCC history. https://www.carbonbrief.org/ongoing-failure-to-agree-ar7-timeline-is-unprecedented-in-ipcc-history/

CRREM. (2023). Carbon Risk Real Estate Monitor: Risk assessment reference guide and global decarbonisation pathways. https://www.crrem.eu/

Deloitte. (2022). Comparing the ECB SSM climate stress test and the Bank of England's CBES. https://www.deloitte.com/uk/en/services/audit-assurance/blogs/comparing-the-ecb-ssm-climate-change-stress-and-the-bank-of-englands-cbes.html

European Central Bank. (2022). 2022 climate risk stress test: Methodology, scenarios and quality assurance. https://www.bankingsupervision.europa.eu/ecb/pub/pdf/ssm.climate_stress_test_report.20220708~2e3cc0999f.en.pdf

European Central Bank. (2025). Integrating climate risk into the 2025 EU-wide stress test (Macroprudential Bulletin). https://www.ecb.europa.eu/press/financial-stability-publications/macroprudential-bulletin/html/ecb.mpbu202511_04.en.html

EY. (2023). What you need to know about new ISSB standard IFRS S2. https://www.ey.com/en_us/insights/ifrs/what-you-need-to-know-about-new-issb-standard-ifrs-s2

Greengage Environmental. (2023). CRREM releases new pathways. https://www.greengage-env.com/crrem/

Hausfather, Z., & Peters, G. P. (2020). Emissions: The "business as usual" story is misleading. Nature, 577, 618 to 620. https://doi.org/10.1038/d41586-020-00177-3

IFRS Foundation. (2022). ISSB confirms requirement to use climate-related scenario analysis. https://www.ifrs.org/news-and-events/news/2022/11/issb-confirms-requirement-use-climate-related-scenario-analysis/

IFRS Foundation. (2023). IFRS S2 Climate-related Disclosures. https://www.ifrs.org/

IPCC. (2025). Seventh Assessment Report (AR7): work programme and author selection. https://www.ipcc.ch/assessment-report/ar7/

JBA Risk Management. (2025). How are climate scenarios made? https://www.jbarisk.com/knowledge-hub/insights/how-are-climate-scenarios-made/

Munich Re. (2025). IPCC vs NGFS climate scenarios: What risk managers need to know. https://www.munichre.com/rmp/en/the-re-brief/risk-modelling/ipcc-vs-ngfs-climate-scenarios.html

Network for Greening the Financial System. (2024). NGFS climate scenarios for central banks and supervisors (Phase V). https://www.ngfs.net/ngfs-scenarios-portal/

O'Neill, B. C., Tebaldi, C., van Vuuren, D. P., et al. (2016). The Scenario Model Intercomparison Project (ScenarioMIP) for CMIP6. Geoscientific Model Development, 9, 3461 to 3482.

Riahi, K., van Vuuren, D. P., Kriegler, E., et al. (2017). The Shared Socioeconomic Pathways and their energy, land use, and greenhouse gas emissions implications. Global Environmental Change, 42, 153 to 168.

Sanderson, B. M., et al. (2024). The need for carbon-emissions-driven climate projections in CMIP7. Geoscientific Model Development, 17, 8141 to 8172. https://gmd.copernicus.org/articles/17/8141/2024/

Sanderson, B. M., et al. (2025). flat10MIP: An emissions-driven experiment to diagnose the climate response to positive, zero and negative CO2 emissions. Geoscientific Model Development, 18, 5699 to 5724. https://gmd.copernicus.org/articles/18/5699/2025/

Schwalm, C. R., Glendon, S., & Duffy, P. B. (2020). RCP8.5 tracks cumulative CO2 emissions, and reply to Hausfather and Peters. Proceedings of the National Academy of Sciences, 117(33 and 45). https://www.pnas.org/doi/10.1073/pnas.2017124117

Socious. (2026). What is ISSB? IFRS S1 and S2 explained for sustainability teams. https://www.socious.io/blog/what-is-issb-ifrs-s1-s2-explained/

Sustainability Atlas. (2026). ISSB standards (IFRS S1 and S2): Global sustainability reporting implementation guide. https://sustainableatlas.org/

Taskforce on Nature-related Financial Disclosures. (2023a). Guidance on the identification and assessment of nature-related issues: The TNFD LEAP approach (Version 1.0). https://tnfd.global/

Taskforce on Nature-related Financial Disclosures. (2023b). Discussion paper on conducting advanced scenario analysis. https://tnfd.global/

Tebaldi, C., Debeire, K., Eyring, V., et al. (2021). Climate model projections from the Scenario Model Intercomparison Project (ScenarioMIP) of CMIP6. Earth System Dynamics, 12, 253 to 293.

Van Vuuren, D. P., O'Neill, B. C., Tebaldi, C., et al. (2026). The Scenario Model Intercomparison Project for CMIP7 (ScenarioMIP-CMIP7). Geoscientific Model Development, 19, 2627 to 2656. https://doi.org/10.5194/gmd-19-2627-2026

Zimm, C., Mintz-Woo, K., Brutschin, E., et al. (2024). Justice considerations in climate research. Nature Climate Change, 14, 22 to 30. https://doi.org/10.1038/s41558-023-01869-0

Further reading

- Navigating the RICS Global Standards for ESG in Commercial Property

The RICS 4th edition embeds climate and transition-risk scenarios into Red Book valuation, a downstream disclosure standard directly exposed to a scenario re-base.

- The Hidden Flaw in the World’s Biggest Corporate Climate Plan

Both turn on Science Based Targets initiative and Net Zero pathway design; the SBTi mandate is part of the same transmission chain from climate scenarios into corporate obligation.

- The Sustainability Professional’s Guide to Global Finance

Shares the CRREM stranding, NGFS and climate-risk-as-financial-risk machinery that the re-based scenarios feed; the finance-side next step in the argument.

Related posts

Assessing the Global Military Climate Footprint

The Carbon Ledger of Conflict Geopolitical Blind Spots in Global Climate Frameworks The global effort to mitigate anthropogenic climate change is currently operating with a significant structural deficiency: the systematic omission of military emissions from international governance frameworks. For decades, the global military-industrial complex has functioned within a regulatory blind spot, shielded by geopolitical sensitivities

Carbon Offsets: A Flawed Solution, According to New Research?

Carbon Offsets: A Flawed Solution, According to New Research For years, carbon offsetting has been promoted as a key tool in the fight against climate change. The concept is simple: compensate for emissions by investing in projects that reduce or remove greenhouse gases elsewhere. However, a comprehensive research paper by Joseph Romm, Stephen Lezak, and

World's Top Courts Issue Landmark Rulings on Climate Change

World’s Top Courts Issue Landmark Rulings on Climate Change Two of the world’s most important courts have made major rulings on climate change. In 2024 and 2025, these courts clarified the legal duties that countries have to protect the planet for current and future generations. These landmark opinions create a strong, enforceable legal framework for